AMBREY BRIEFING NOTE –BULK SHIPPING IN THE ARABIAN/PERSIAN GULF

Date issued: 27 April 2026

“Ahead of Geneva Dry next week, Ambrey has conducted research on bulk shipping risk in the Arabian/Persian Gulf, focusing on the situation for bulkers operating in the region. The environment is not a binary “blocked vs open” scenario, but a fragmented risk landscape where operational decisions hinge on imperfect intelligence, fleet economics, and tolerance for coercive enforcement.”

EXECUTIVE SUMMARY

- The total hull market value of the blocked panamax and capesize bulkers in the Gulf is US $1.3bn.

- The US has made an exception to its blockade on Iran for humanitarian cargoes; Iran has not.

- Chinese shipowners without pre-established Iran links are likely blocked; the Iranian blockade is different to the Houthi ‘ban’ on Red Sea navigation in this respect.

- The behaviour of bulkers indicates there could be systematic reasons for shipowners with smaller fleets to accept greater risk.

- Blockade messaging and practical application makes charter party disputes almost inevitable.

Blocked in the Gulf?

Since the start of the conflict on 28 February 2026, Ambrey has recorded 126 panamax and capesize bulkers operate inside the Gulf. Not all of these should be considered to be ‘blocked’.

Iran-links

There appears to have always been an exception made for Iran-owned shipping. All the Iranian-owned bulkers at the time of writing were owned by the Islamic Republic of Iran Shipping Lines Company (IRISL). This was a sanctioned entity.

In the early weeks of the conflict, some bulkers that had called Iran were also waiting inside the Gulf. This indicated that whilst they had permission to deliver cargo to Iran, they did not have permission to depart the Gulf once they had discharged their cargo. This observation was recorded in an Ambrey Port Risk Assessment for Bandar Imam Khomeini dated 9 March 2026 and evidenced by an attack on STAR GWYNETH on 11 March 2026 as she was headed toward the Strait of Hormuz, after having called the same port.

Departures from the Gulf by Iran-linked bulkers indicate that by 15 March 2026, this had changed. No Iran-linked bulkers have since reported an attack. At the time of writing this report, Ambrey assessed that 50 bulkers with Iranian ownership or port calls had operated inside the Gulf during the conflict, and that 18 bulkers remained in the Gulf. Ambrey assesses that these vessels are not ‘blocked’.

US blockade

The stated scope of the US blockade has changed over time:

On 12 April 2026, President Trump announced on Truth Social that the blockade would apply to the Strait of Hormuz, and that he had instructed the Navy to interdict vessels that has paid a toll to Iran: “The United States Navy…will begin the process of BLOCKADING any and all Ships trying to enter, or leave, the Strait of Hormuz.” Adding, “I have also instructed our Navy to seek and interdict every vessel in International Waters that has paid a toll to Iran. No one who pays an illegal toll will have safe passage on the high seas.”

US CENTCOM’s subsequent statement the same day was considerably narrower in scope: “U.S. CENTCOM forces will begin implementing a blockade of all maritime traffic entering and exiting Iranian ports on April 13 at 10 a.m. ET, in accordance with the President’s proclamation. The blockade will be enforced impartially against vessels of all nations entering or departing Iranian ports and coastal areas, including all Iranian ports on the Arabian Gulf and Gulf of Oman. CENTCOM forces will not impede freedom of navigation for vessels transiting the Strait of Hormuz to and from non-Iranian ports.”

The US blockade would not therefore apply to all merchant vessels, only to vessels calling Iranian ports.

On 12 April, Ambrey sought clarification from the US whether the blockade of Iranian ports would include bulk grain shipments. The US Navy confirmed on 13 April that “Humanitarian shipments including food, medical supplies, and other goods essential for survival of the civilian populations will be permitted, subject to inspection.” Later on 13 April, Ambrey recorded a US VHF radio broadcast in the Gulf of Oman stating: “Do not attempt to breach the blockade. Vessels will be boarded for interdiction and seizure transiting to or from an Iranian port. If you do not comply with this blockade, we will use force.” Therefore, the US Navy may compel inspection, and a merchant vessel may be damaged if it does not comply.

Ambrey does not assess a bulker to be ‘blocked’ by the US, even if it has called an Iranian port, provided its cargo can be considered “humanitarian”. Foodstuffs would qualify.

Intraregional trade

Several bulkers regularly trade within the Gulf, and have continued to do so. The most common port call pairing is between Saqr, UAE, and Shuaiba, Kuwait. This is primarily serviced by the Kuwaiti Combined Group Rocks Company K.S.C.C., and the Emirati Al Khalejia Aggregates FZE. Some of their vessels would ordinarily call Fujairah, UAE and Sohar, Oman, which has largely stopped. However, vessels have continued to transit within the Gulf. Therefore, if they have been blocked, they have not been blocked in the same way that global bulk operators have.

Non-Iranian global operators blocked in the Gulf

Ambrey assesses that 51 panamax and capesize bulkers remain almost certainly ‘blocked’

Rather than reacting to incidents as they emerge, Ambrey forecasts exposure, assesses new routes and ports, identifies evolving threat patterns, and develops tailored mitigation frameworks well in advance of execution. This forward visibility enables a fundamentally different level of preparation. Risk management becomes structured and predictive, rather than reactive. When events occur, they are assessed against an established baseline, allowing clients to identify deviations from normal operating patterns rather than reacting to isolated signals.

Market value

The total market value of those blocked is estimated to be US $1.3 billion. The average values by size are carried below:

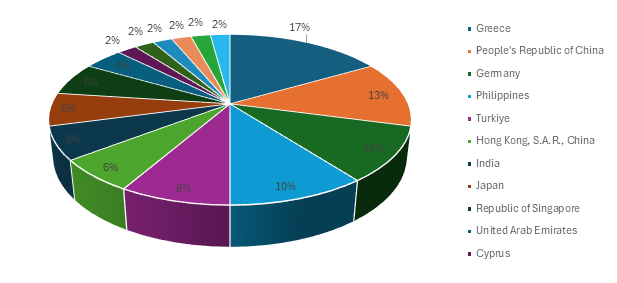

Shipowner nationality

During the Red Sea crisis, the Houthis almost certainly avoided targeting Chinese-owned shipping. The ‘Humanitarian Operations Coordination Centre’ (HOCC) would deconflict and issue a guarantee of safe passage to shipping. The behaviour of bulkers inside the Gulf indicates that Chinese owners (Hong Kong S.A.R. included) have not been given similar assurances.

Attempts to depart

On 17 April 2026, the Iranian Ministry of Foreign Affairs stated the transits were permitted “on the coordinated route as already announced by Ports and Maritime Organisation of the Islamic Rep. of Iran”. Within an hour of this statement, the US President announced that the US blockade was still operational. Between 17-18 April, nine otherwise ‘blocked’ panamax and capesize bulkers attempted to depart the Gulf. All turned around amid Iranian threats, and attacks on other types of merchant vessels on 18 April. No bulkers were damaged.

On 17 April, Ambrey adopted a cautious approach, issuing the following guidance: “Whether all shipping is permitted to transit freely is unanswered. The Iranian Foreign Minister has not always been backed in the statements by Iranian hardliners. If an attempt to transit is made, vessels are advised to remain clear of the Traffic Separation Scheme and to abort the transit by returning to the point of origin as soon as threatened over VHF.”

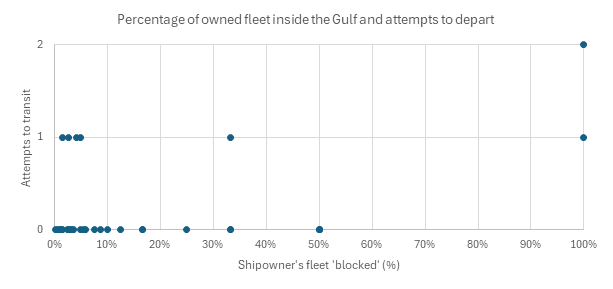

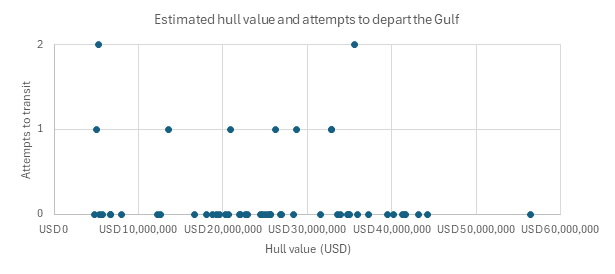

Few of those ‘blocked’ attempted a transit. Ambrey found a moderate positive correlation between the proportion of ships in a shipowners’ fleet that were ‘blocked’, and transit attempts. There was a very weak negative correlation between hull value and an attempt to transit.

r=0.5

r=-0.1

This indicates a need for greater research on the economics of risk management. This includes:

- Are there differences in information sources between shipowners with larger and smaller fleets?

- Can charterparty agreements, or the lack thereof, explain the discrepancies?

- Are some of the shipowners with smaller fleets and blocked in the Gulf facing cashflow issues?

- Had more shipowners with smaller fleets located their bulkers off the UAE, closer to the Strait of Hormuz, such that they could take advantage of an opening?

Incidents

During the conflict, four bulk carriers have been damaged. Two were damaged whilst outbound from the Gulf, headed towards the Strait of Hormuz. A third was subject to collateral damage in the Gulf of Oman, a fourth reporting a suspicious explosion nearby when northeast of Oman, and a fifth suffered damage in unexplained circumstances east of Oman.

Shipping in the Gulf

The only vessels damaged inside the Gulf were in transit outbound.

02:05 UTC 11 March 2026 Transiting towards the Strait of Hormuz, eastbound

A Marshall Islands flagged, panamax Greek-owned bulk carrier was damaged whilst in transit towards the Strait of Hormuz, 50NM northeast of Dubai, UAE. An aerial projectile caused a 2m hole to cargo hold 1 and damage to ballast tanks. As a consequence of the strike, the vessel began to list. All crew were reported safe and accounted for. The vessel’s AIS was on at the time, but there were indications of GNSS interference. The bulker had last called Bandar Imam Khomeini, Iran. It was assessed likely this was a deliberate targeting of the vessel for attempting a non-approved transit. The vessel proceeded under her own power to Duqm shipyard for repairs, where she remained on 23 April 2026. This was assessed to be a partial loss.

04:35 UTC 11 March 2026 Transiting the Strait of Hormuz, eastbound

A Thailand-flagged handysize bulk carrier was struck by two projectiles while transiting the Strait of Hormuz destined for Kandla, India, approximately 25NM north-northeast of Khasab, Oman. The strike resulted in a fire onboard the vessel. Twenty crew members were evacuated from the vessel initially, and three others, all engine room personnel, were reported missing, later reported as fatalities. The vessel had entered the Arabian/Persian Gulf on 28 February 2026 an hour after the IRGC had announced the Strait of Hormuz closed, and had been waiting in an anchorage northwest of Jebel Ali prior to attempting the transit outbound. The owner and manager claimed: “Based on the information and maritime security advisories available at that time, the vessel was assessed as suitable to undertake the transit with appropriate precautionary measures in place. The vessel’s officers and crew were informed of the prevailing security situation in the region and the passage…the Company determined that proceeding with the transit through the Strait of Hormuz with enhanced security precautions was the appropriate course of action at that time”. It was unclear from the reporting what professional advice the owner and manager had engaged. According to the owner and manager, they had remained in regular contact with the UKMTO and Royal Thai Navy prior to and during the attempted transit. There were no reports of any coordination with the Iranian authorities prior to the transit. The vessel reportedly later ran aground on Qeshm Island, Iran. It was assessed to be a total loss.

Considerations for the industry

These are prompts designed for hypothetical panel discussions.

Humanitarian cargo treatment:

- Does the US assurance of permitting humanitarian cargoes assuage industry concerns in shipping non-sanctioned bulk products to/from Iran?

- Does industry hold the US to a higher standard than Iran on allowing humanitarian cargoes?

- Are we seeing the development of a parallel fleet even in unsanctioned sectors?

- Should industry demand formal, pre-cleared transit mechanisms rather than post-hoc inspection rights?

- Is the industry prepared to reach or even advocate for an agreement on bulk shipments ahead of more sensitive shipments?

Bulk shipments after this crisis:

- At what disruption threshold does diversion away from the Strait of Hormuz become viable—not just discussed?

- Can Eastern Mediterranean / Red Sea / Oman corridors realistically absorb capesize/panamax volumes?

- Are we talking about true substitution or just partial, high-cost workarounds?

- Who wins: regional ports, rail operators, or smaller vessel segments?

- Does crisis accelerate a permanent re-routing of bulk trade flows?

Decision-making under ambiguity:

- Are large fleets structurally better informed – or just more risk-averse?

- How much do owners rely on private intelligence vs state advisories?

- When signals conflict, what actually drives the “go / no-go” call?

- Are charterparty frameworks fundamentally misaligned with fluid, undeclared conflict zones?

- Should there be an industry standard for “minimum intelligence thresholds” before transit?

Cashflow and risk management:

- Do delayed insurance payouts make risk-taking economically rational for smaller owners?

- Is current war risk insurance designed for loss events, not revenue paralysis?

- How should owners price the cost of waiting vs the risk of a failed transit?

Ambrey: +44 203 503 0320, intelligence@ambrey.com

AMBREY – For Every Seafarer, Every Vessel, Everywhere.