AMBREY INSIGHT> THE FLAG IN THE CROSSFIRE: HOW PANAMA-FLAGGED SHIPS BECAME BEIJING’S PRESSURE POINT

Date issued: 08 May 2026

“Since 8 March 2026, and continuing, China has detained Panama-flagged merchant vessels at unprecedented rates, framed as port state control (PSC). The pattern coincides with a Panamanian Supreme Court ruling that stripped Hong Kong-based CK Hutchison of its concession over two Panama Canal terminals. It now sits at the centre of a wider US–China contest over canal access and port ownership. For shipowners, charterers, and the underwriters behind them, the pattern has converted a routine compliance regime into a source of acute, flag-specific operational risk.”

EXECUTIVE SUMMARY

- In March 2026, 93 of 125 vessels detained in Chinese ports were Panama-flagged: about 74% of all China detentions, against 23 in January and 20 in February. The pace accelerated in April, with 136 Panama-flagged vessels detained in Chinese ports, accounting for 91% of all Panama-flagged detentions across the 22-state Tokyo MOU region.

- The surge began on 8 March, reportedly under verbal instructions from Chinese authorities to intensify inspections of Panama-flagged tonnage.

- The US Federal Maritime Commission (US FMC) assesses the inspections appear intended to punish Panama for the loss of CK Hutchison’s port concessions. Beijing rejects this characterisation, holding that the Panamanian court ruling was itself driven by US pressure rather than independent legal process.

- Detentions cite technical deficiencies (fire safety, lifesaving, MARPOL, and ISM gaps) and typically last one to five days, but disrupt rotations and raise costs.

- The detention surge sits within a broader Chinese response that also includes COSCO’s suspension of container services at Balboa, the summoning of Maersk and MSC executives to Beijing, and the halt of new Chinese investment in Panama.

- No mass reflagging from Panama has yet occurred. However, Chinese leasing companies are now requiring shipowners to reflag away from Panama as a condition of newbuilding finance, with longer-term implications for the registry.

CONTEXT

Friction over the canal ports has built since President Trump’s January 2025 inauguration. He repeatedly accused Beijing of “running” the canal and demanded reduced Chinese influence over a waterway carrying about 5% of global maritime trade. This is consistent with his administration’s broader Hemispheric strategy. Beijing’s stated position throughout the subsequent dispute has been that the Panamanian Supreme Court ruling against CK Hutchison was the product of US pressure on the Mulino government, not independent Panamanian legal process. The US, Panama, and the court itself have rejected that framing, but it informs how Beijing has chosen to respond.

The dispute’s commercial origins date to March 2025, when CK Hutchison agreed in principle to sell 80% of its global ports portfolio (43 terminals, including Balboa and Cristóbal) to a BlackRock-led consortium with MSC’s Terminal Investment Limited (TiL) for roughly US$22.8 billion. Beijing reacted sharply, opening an antitrust review that stalled closure. CK Hutchison invited state-owned COSCO into the consortium to placate Beijing but talks remained unresolved through 2025.

In parallel, Panama’s Comptroller General, Anel Flores, audited the 1997 concession and the 2021 extension, alleging unpaid dues and tax exemptions that cost the state roughly US$1.3 billion. On 30 January 2026, the Supreme Court voided both the original Law 5 and the 2021 extension; Beijing condemned the ruling as an “act of bad faith.” On 23 February, the government occupied the two terminals and assigned interim 18-month operations to APM Terminals (Balboa) and TiL (Cristóbal). CK Hutchison rejected the takeover as unlawful and, on 24 March, escalated the matter to International Chamber of Commerce arbitration, seeking damages exceeding US$2 billion.

Beijing’s response unfolded across several channels. The Ministry of Transport and the National Development and Reform Commission summoned Maersk and MSC executives to Beijing on 9–10 March, and later demanded both companies “immediately” withdraw from Balboa and Cristóbal. Both have continued operating, with the carriers arguing that any withdrawal would simply transfer the terminals to US firms. On 10 March, COSCO Shipping Lines suspended its container services at Balboa. State-owned firms were directed to pause new investments in Panama, including the Fourth Bridge over the canal. From 8 March, Chinese MSA officers began holding Panama-flagged vessels at unusually high rates, as set out below. On 7 April, Premier Li Qiang signed a State Council order expanding Beijing’s authority to retaliate against foreign regulatory actions deemed harmful to Chinese interests.

ANALYSIS

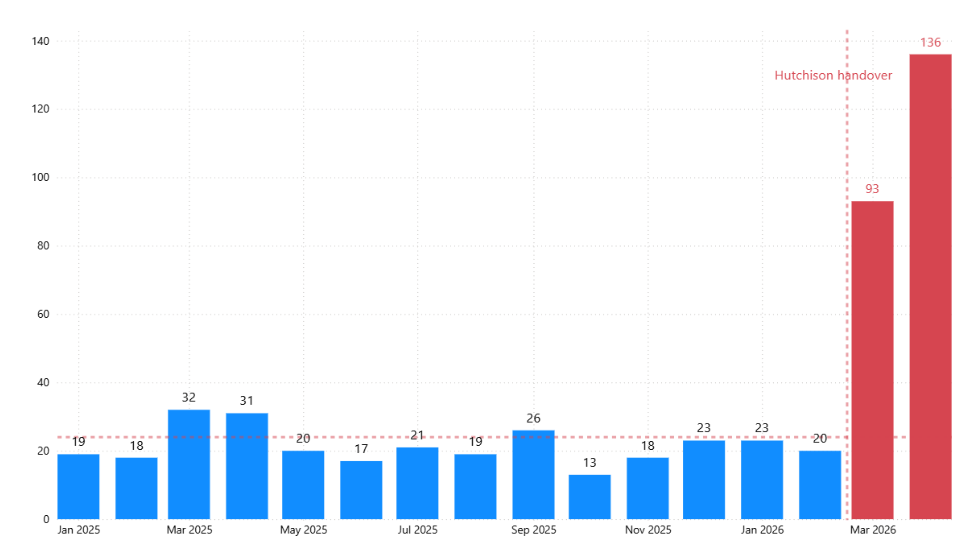

The most striking feature of the March–April 2026 dataset is the scale of the departure from prior monthly norms. Tokyo MOU Detention List records show that Panama-flagged detentions in Chinese ports averaged 21 per month across 2025 and peaked at 32 in March 2025. The first two months of 2026 sat firmly within this band, at 23 and 20 respectively. From March 2026, the monthly count moved to an entirely different scale.

Figure 1: Panama-flagged vessel detentions in Chinese ports, monthly from January 2025 to April 2026

Source: Ambrey’s analysis of the Tokyo MOU Detention List (Memorandum of Understanding on Port State Control in the Asia-Pacific Region), January 2025 – April 2026. Note: The vertical marker indicates the 23 February 2026 transfer of the Hutchison-operated terminals to APM Terminals (Balboa) and TiL (Cristóbal). The Tokyo MOU covers 22 maritime authorities across the Asia-Pacific.

Figure 1 shows the shift clearly. Across the 14 months from January 2025 to February 2026, the bars cluster between 13 and 32 detentions per month, a band the trade had long treated as routine, including seasonal noise around Chinese New Year and post-East Asian monsoon survey cycles. From March 2026, the bars jump to a different scale entirely: 93 in March, 136 in April. The dashed reference line marks the 2025 monthly average of 21; the vertical marker indicates the 23 February 2026 transfer of the Hutchison-operated terminals. Two features of the profile stand out. First, the shift inflection is sharp and unambiguous: March was 4.3 times the 2025 monthly average and nearly three times the previous peak (32 in March 2025), while April was 6.4 times the 2025 average. Second, Panama’s share of all China detentions also widens, from a historical band of 22%–43% across 2016–2025 to 74% in March and 82% in April. No comparable surge has been recorded against any other major flag in the same window.

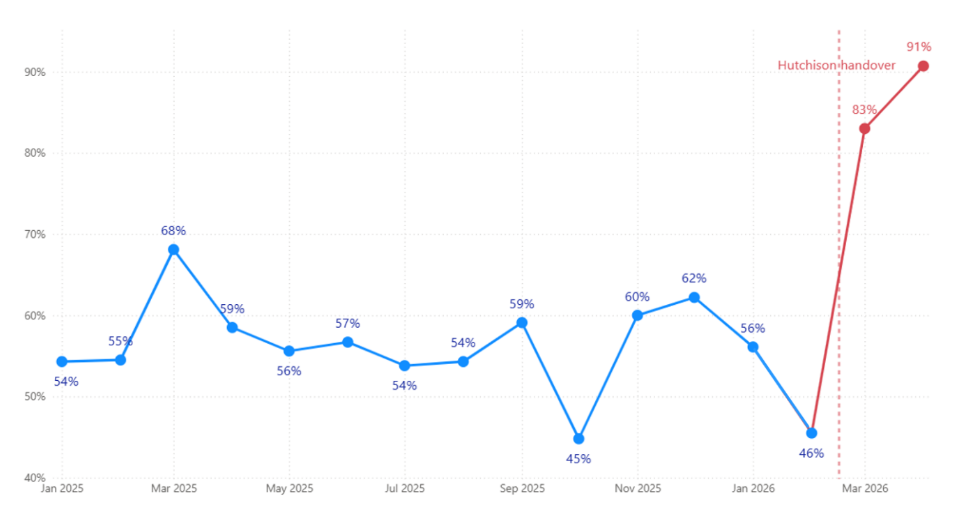

The same concentration is visible in geography.

Figure 2: Share of Tokyo MOU Panama-flagged detentions occurring in Chinese ports, monthly from January 2025 to April 2026

Source: Ambrey’s analysis of the Tokyo MOU Detention List (Memorandum of Understanding on Port State Control in the Asia-Pacific Region), January 2025 – April 2026. Note: Vertical marker indicates the 23 February 2026 transfer of the Hutchison-operated terminals to APM Terminals (Balboa) and TiL (Cristóbal). The Tokyo MOU covers 22 maritime authorities across the Asia-Pacific.

Figure 2 closes off the most plausible alternative explanation: that the surge reflects deteriorating Panama-flagged fleet quality. If that were the case, Panama-flagged detentions would rise across the whole Asia-Pacific region in lockstep, and China’s share of those detentions would stay roughly constant. Instead, the share moves from a noisy 12-month band of 45%–68% (averaging 57% across 2025) to 83% in March 2026 and 91% in April. February 2026, at 46%, was actually the lowest reading in 16 months, which makes the subsequent two-month jump of more than 45 percentage points all the more striking. By April, virtually every Panama-flagged vessel detained anywhere in the Tokyo MOU region was held in a Chinese port. The change is concentrated in time, in flag, and in geography. Any fleet-quality explanation would need to account for all three at once.

The detentions are formally framed as routine port state control. The deficiencies cited mirror those highlighted in the Panama Maritime Authority’s MMN-06/2026 advisory: fixed fire-extinguishing installations, remote means of control for machinery spaces, lifeboats, ventilators, and ISM maintenance gaps. On their own these are common findings, but the Tokyo MOU classifies Panama as a low-risk flag (status valid through 30 June 2026). The Chinese Foreign Ministry declined to confirm targeting on 28 March; spokesperson Lin Jian later called the US-led joint statement of 28 April a “smear,” reiterating that the underlying canal dispute reflected US attempts to control the waterway. Panama’s Vice Foreign Minister Carlos Hoyos called the surge disproportionate to historical norms, and President Mulino described it as a political signal. On 28 April, six governments (the US, Bolivia, Costa Rica, Guyana, Paraguay, and Trinidad and Tobago) issued a joint statement backing Panama’s sovereignty.

IMPLICATIONS

Against this politicised backdrop, the operational consequences fall on a commercial register that does not align with political allegiances. The surge creates a real cost premium for Panama-flagged calls at Chinese ports. Some Chinese-controlled carriers operating under the Panama flag appear in the Tokyo MOU Detention List themselves, so ownership nationality offers no reliable mitigation. The detained fleet still skews older, but not disproportionately to those that called China which were 16 years or older, indicating that age alone was not the focus of Chinese inspections. Over 4,600 Panama-flagged vessels called at Chinese ports in 2025, indicating a large exposed fleet. There were no reports of mass reflagging away from Panama at the time of writing.

The more durable threat is structural. Chinese leasing companies are reportedly requiring shipowners to reflag away from Panama as a condition of newbuilding finance. Chinese yards built most of the new tonnage entering the global fleet in 2024 and 2025, so this finance-side condition could erode Panama’s newbuild intake more effectively than any inspection regime, redirecting future fleet growth toward competing registries.

The supply-chain disruption is concrete. Tokyo MOU rules require all cited deficiencies to be rectified before a vessel sails, so even an average one-to-five-day hold breaks liner rotations, crew rotations, and onward cargo connections; longer cases occur, with some Panama-flagged vessels held for around eight days, according to the Tokyo MOU Detention List. Clearance at one Chinese port does not insulate a vessel from re-inspection at the next, and where a detention is classified as a government action, cargo interests may have limited recourse against the carrier. Rerouting follows two patterns: carrier-led, where COSCO has redirected empty containers from Balboa to Manzanillo and Colón and shifted transhipment cargo to Lázaro Cárdenas (Mexico) and Buenaventura (Colombia); and cargo-led, where forwarders are pre-screening Panama-flagged tonnage’s PSC history and switching bookings to other flags (most often Liberia) before cargo reaches the Chinese dock.

The US FMC retains authority to investigate foreign government practices that disadvantage US trade. Strategically, the episode shows that flag-state status, long treated as an administrative formality, has acquired strategic weight that operators can no longer ignore.

RECOMMENDATIONS

Operators with Panama-flagged tonnage calling Chinese ports should consider the following:

- Pre-arrival rectification. Treat the PMA’s MMN-06/2026 as a working checklist. Address fire safety (07109, 07114, 07199), lifeboats (11101), ventilators and air pipes (03108), and ISM items (15109, 15150) before arrival, with documentary evidence of closure.

- Class engagement and scheduling buffers. Coordinate with class to verify recent surveys, certificates, and ballast-water-management compliance, with attention to MARPOL Annex I and VI items recurrent in the China pattern. Build one-to-five-day contingency into rotations involving Chinese ports, and review demurrage, off-hire, and consequential-loss exposures.

- Flag risk review. For tonnage with high China call frequency, run a documented commercial assessment of reflagging options against the time, cost, and counterparty implications. Operators of older tonnage should expect tighter vetting at alternative registries, so reflagging will not be a quick fix.

- Use of appeal mechanisms. Where detentions appear unsupported by the cited deficiencies, exercise the Tokyo MOU appeal and review process via the flag administration.

- Monitoring. Track Tokyo MOU disclosures, US FMC statements, Chinese Ministry of Transport announcements, and Panamanian Foreign Ministry communiqués. The dispute remains live across diplomatic, legal, and commercial channels.

Ambrey assesses that the elevated detention rate will persist while the underlying canal-port dispute remains unresolved. The Chinese government’s late-April acknowledgement that the matter is in international arbitration suggests possible de-escalation. However, the structural drivers, including the contested CK Hutchison portfolio sale, Panama’s transition from interim to permanent concession arrangements, new finance-related reflagging conditions, and competing US and Chinese positions on influence in the Western Hemisphere, point to a multi-quarter horizon. Operators should consider their exposure accordingly.

CONTACT INFORMATION

Ambrey: +44 203 503 0320, intelligence@ambrey.com

AMBREY – For Every Seafarer, Every Vessel, Everywhere.